Higher super contribution caps from 1 July 2026: What it means for you

From 1 July 2026, the amount you can contribute to super will increase, creating new opportunities to boost your retirement savings.

The annual concessional contribution cap will rise from

$30,000 to $32,500. These are contributions made from pre-tax money, such as employer contributions, salary sacrifice and personal deductible contributions.

Non-concessional contributions

The annual non-concessional contribution (NCC) cap will also increase from $120,000 to $130,000. These are contributions made from your after-tax money.

For people who are eligible to use the bring-forward rule, the higher caps will allow even larger contributions. From 1 July 2026, the three-year bring-forward cap will increase from $360,000 to $390,000.

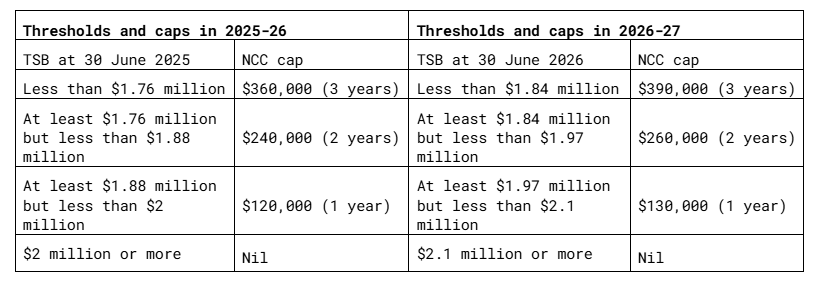

Whether you can use these higher NCC caps will depend on your total super balance (TSB) at 30 June 2026. Your TSB is the total amount you have across all of your super accounts at that date, including money in accumulation and pension phase.

The table below highlights how the TSB thresholds and NCC caps will change from 2025–26 to 2026–27:

One important trap to watch is that if you have already triggered a bring-forward period before 1 July 2026, you do not get access to the new higher caps for that existing period. For example, if you triggered a three-year bring-forward in 2025–26, you remain limited to the current maximum of $360,000 across that three-year period, being until 1 July 2028. You do not get to use the new $390,000 cap.

Concessional contributions

The higher concessional cap may also create extra opportunities through catch-up concessional contributions. If your TSB is less than $500,000 at 30 June of the previous year, you may be able to use unused concessional cap amounts from the previous five years. In some cases, this could allow a very large deductible contribution to be made.

This means the lead-up to 30 June 2026 could be an important planning window. In some cases, it may make sense to delay a contribution until the new financial year to access the higher caps. In others, if you have already met a condition of release, taking a small amount out of super before 30 June may help keep your balance below a key threshold and preserve access to valuable contribution strategies.

The key message is that the higher caps could create valuable opportunities, but the rules around timing and TSB are also important. Now is a good time to check how these changes may apply to you.

Previous Blog Posts: