Using super to pay the mortgage

Have you reached preservation age and still have a mortgage? If so, you may be able to use your super to deal with your rising mortgage repayments if you meet certain conditions.

Introduction

The constant increase to interest rates over the last two years have left some borrowers strapped for cash. Fortunately, those that have reached preservation age can access their superannuation via a special type of pension, known as a transition to retirement (TTR) pension, even if they haven’t retired.

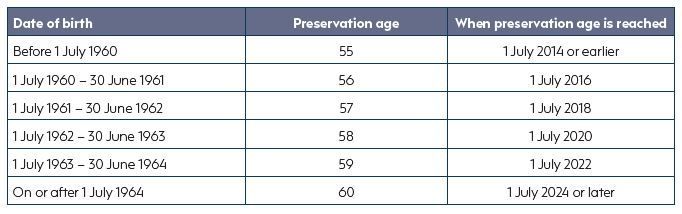

What is preservation age?

Your preservation age is the earliest age you can access your superannuation. The preservation age that applies to you depends on your date of birth and ranges from age 55 to 60, as shown in the table above.

Alternatively, you will also reach preservation age when you reach age 65, even if you are still working.

What is a TTR pension?

A TTR pension allows you to supplement your income by allowing you to access some of your superannuation once you’ve reached your preservation age. You can start a TTR pension by transferring some of your superannuation to an account-based pension (ABP), which is a regular income stream bought with money from your superannuation fund.

Once you start a TTR pension, you need to withdraw payments between a minimum and maximum range each year. The minimum drawdown rate depends on your age and is 4% for those under 65 years old. The maximum amount you can withdraw is 10% of your account balance as at 1 July of each financial year (or 10% of the value from the date your TTR pension started in that financial year). This means you can choose pension payments anywhere between your minimum and maximum payment limit each year.

Tip – if you commence a TTR pension halfway through the year, the minimum payment percentage is pro-rated to reflect the number of days the pension is in place in that first financial year. The minimum will be recalculated at 1 July based on your TTR pension balance and your age at that time to factor in a whole year’s worth of pension payments.

But note that a TTR pension does not allow you to withdraw your superannuation as a lump sum. This can generally only be done once you’ve reached your preservation age and met certain conditions of release, such as retirement.

Example

Justine is 60 years old and has $650,000 in superannuation. Justine’s adviser recommends she commences a TTR pension with $600,000 to help ease her financial difficulties. Justine must draw a minimum of $24,000 (ie, 4% x $600,000) or up to a maximum of $60,000 (ie, 10% x $600,000) in pension payments in the 2023-24 financial year.

Justine can use the additional TTR pension payments to help supplement her employment income and meet her mortgage repayments. She could also use a TTR pension as a strategy to pay down her mortgage much quicker than planned even if she could easily afford her repayments.

Factors to consider

- If you are 55 to 60, the taxable amount of your income from your TTR pension is taxed at your marginal tax rate, less a 15% tax offset.

- Once you turn 60, your TTR pension payments are all tax free.

- Any investment earnings generated from your TTR pension are subject to the same maximum 15% tax rate as superannuation accumulation funds.

- Once you reach age 65 or retire, your TTR pension will automatically convert to an ABP. This means more flexibility as the 10% maximum pension limit will no longer apply.

Need help?

You should seek financial advice before deciding if a TTR pension is right for you as it could help you understand the possible benefits and implications for your particular circumstances.

Previous Blog Posts: